Accounting

Preparation of Financial Statements

Adjustments to Financial Statements

🤓 Study

📖 Quiz

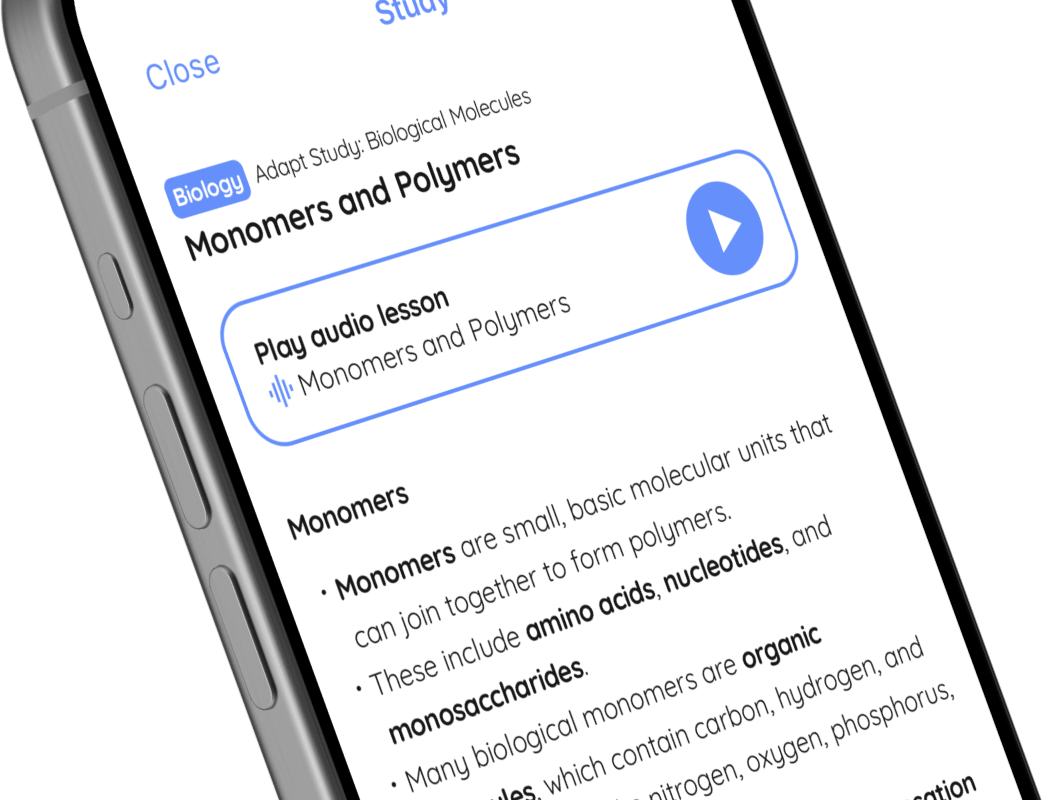

Play audio lesson

Adjustments to Financial Statements

Understanding Adjustments to Financial Statements

- Adjustments to financial statements are typically applied at the end of a financial period.

- This process can include profit and loss items and balance sheet items, such as stock valuations, accruals, and prepayments.

- Adjustments are necessary to reflect the true and correct financial position of a business and to ensure accounting standards are met.

Common Types of Adjustments

Accruals

- Accruals are expenses that a business has incurred but not yet paid for.

- When preparing financial statements, these expenses need to be added in the current period, increasing both the expenses and liabilities in the balance sheet.

Prepayments

- Prepayments refer to payments for services or goods which the business will receive in the future.

- Prepaid amounts are first recorded as an asset, but over time as the goods or services are received, the asset is reduced and the amount becomes an expense.

Depreciation

- Depreciation is used to spread the cost of a tangible fixed asset over its useful life.

- This is particular is a non-cash adjustment that involves increasing depreciation expense and reducing the balance of the asset account.

Bad debts and provision for doubtful debts

- Bad debts are accounts receivable that a firm is unlikely to collect, and thus becomes an expense.

- The provision for doubtful debts is a precautionary amount set aside for possible non-collection of receivables.

Adjustments process

- When making adjustments to financial statements, a business would first need to identify the nature of each transaction and determine if an adjustment is needed.

- Any adjustments should be documented in the journal entries, with a clear explanation of the reason for each change.

- These will then need to be posted to the ledger accounts, debiting and crediting appropriately.

- Finally, reflect the adjusted amounts in the finalised financial statements.

Importance of adjustments

- Ensures the business' financial position is accurately presented, aiding in decision-making.

- Adjustments align accounting records with actual business transactions and events.

- Helps to maintain compliance with accounting policies as per GAAP or IFRS.

- Presents a realistic picture of the business to potential investors and shareholders.

- Provides a basis for comparison across financial periods.